Australia Data Center Construction Market Projected to Reach USD 2.29 Billion by 2034

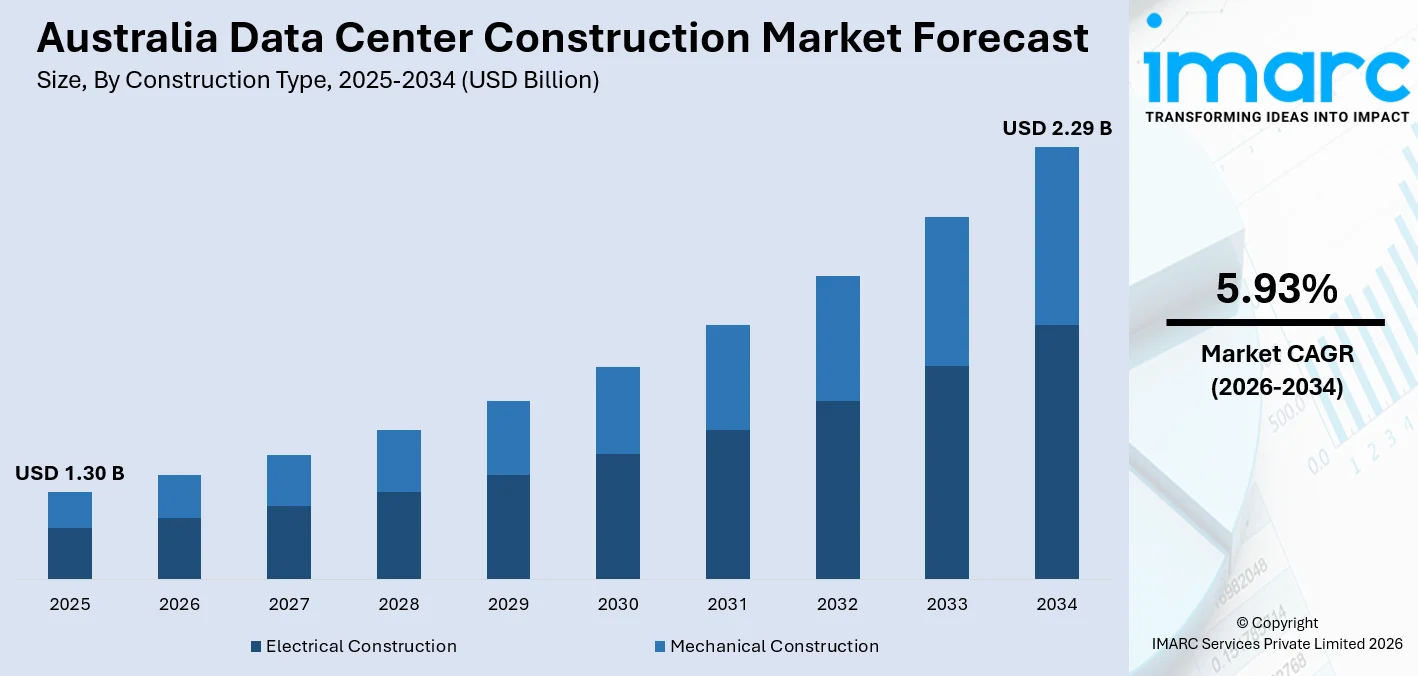

The Australia data center construction market size, valued at USD 1.30 Billion in 2025, is projected to reach USD 2.29 Billion by 2034, growing at a CAGR of 5.93% from 2026-2034.

Australia Data Center Construction Market Overview

Australia Data Center Construction Market Overview

The Australia data center construction market is experiencing unprecedented growth, driven by explosive AI workload demand, massive hyperscale and cloud provider investment commitments, the rapid expansion of colocation capacity, critical power infrastructure development, and the country's emergence as the Asia-Pacific region's second most attractive data centre investment destination after the United States. The Australia data center construction market size was valued at USD 1.30 Billion in 2025, reflecting the intensity of construction activity required to support the nation's digital infrastructure expansion. Australia's total data centre occupancy expanded from 37 MW in 2005 to 1.3 GW in 2025, with deployable capacity projected to more than double to over 3,100 MW by 2030, requiring approximately AUD 26 billion in new investment. Electrical construction dominates at 55.7% of the market, driven by the critical power and cooling infrastructure requirements of modern high-density facilities. Large data centres represent 44.3% by facility type, while Tier III facilities — offering concurrent maintainability — command 46.8% by tier standard. The IT and telecommunications vertical leads at 31.9% market share, supported by 80% of Australian businesses planning cloud migration within two years. Australian Capital Territory and New South Wales account for 37.4% of the market, with Sydney's pre-committed capacity reaching 72% of new supply as hyperscale customers drive approximately 80% of new demand. Between 2023 and 2025, companies announced data centre investments in Australia that could scale up to more than AUD 100 billion, with data centres currently consuming 5% of national electricity generation — projected to reach 8% by 2030.

Looking forward, the Australia data center construction market is projected to reach USD 2.29 Billion by 2034, growing at a CAGR of 5.93% from 2026-2034. This growth trajectory is being supported by transformative investment commitments from global technology giants, institutional investor acquisitions, and domestic operator expansion programs. Amazon committed AUD 20 billion by 2029 to expand Australian data centre infrastructure, while Microsoft pledged AUD 5 billion for cloud and AI capacity. In September 2024, Blackstone acquired AirTrunk — Australia's largest data centre operator — for AUD 24 billion, validating the sector's earnings potential. In December 2025, OpenAI partnered with NEXTDC to build a AUD 7 billion large-scale computing cluster in Sydney, accelerating AI infrastructure deployment. NEXTDC commenced construction on its 550 MW S7 Sydney campus with capacity delivery through 2029, while the M4 Melbourne campus represents a AUD 2 billion investment announced in June 2025. CDC Data Centers broke ground on a hyperscale campus in Western Sydney's Marsden Park set to become the Southern Hemisphere's largest data centre. Partners Group invested AUD 1.2 billion in GreenSquareDC, while Amazon announced a AUD 750 million Brisbane facility in March 2026. The Victorian government fast-tracked NEXTDC's Port Melbourne campus, valued at approximately AUD 2 billion, reflecting state-level recognition of data centre infrastructure as critical economic development. Construction costs in Sydney range between AUD 10-11 per watt and in Melbourne AUD 9.50-10 per watt, while modular construction methods are compressing build timelines by up to 30%.

Request for a sample copy of this report: https://www.imarcgroup.com/australia-data-center-construction-market/requestsample

How AI is Reshaping the Future of the Australia Data Center Construction Market

Artificial intelligence is simultaneously the primary demand catalyst and a transformative construction methodology for Australia's data centre industry, with AI workloads driving unprecedented power density requirements while AI-powered tools revolutionise facility design, construction management, and operational optimisation. AI adoption has the potential to contribute AUD 600 billion annually to Australia's GDP by 2030, creating massive infrastructure demand. Key developments include:

• AI Workloads Driving Unprecedented Power Density and Facility Design Innovation: The explosive growth of AI training and inference workloads is fundamentally reshaping data centre construction specifications, as GPU-intensive computing requires power densities of 30-60+ kW per rack — compared to traditional 5-10 kW per rack for conventional IT workloads — with emerging configurations reaching 80+ kW per rack. This 6-10x increase in power density is driving radical facility design innovation, requiring higher-capacity electrical infrastructure, advanced liquid cooling systems, and more sophisticated heat rejection capabilities. OpenAI's AUD 7 billion partnership with NEXTDC to build a large-scale computing cluster in Sydney exemplifies the scale of AI-specific infrastructure demand, while Amazon's AUD 20 billion commitment and Microsoft's AUD 5 billion pledge are substantially driven by AI and machine learning capacity requirements.

• AI-Powered Construction Planning and Building Information Modelling: AI and machine learning are transforming data centre construction planning by enhancing Building Information Modelling (BIM) with predictive analytics, clash detection, and construction sequencing optimisation. AI-powered BIM systems can simulate thousands of design configurations to identify optimal electrical and mechanical layouts, predict construction conflicts before they occur, and generate construction schedules that minimise critical path duration. Modular construction methods — increasingly designed using AI-optimised prefabrication processes — are compressing data centre build timelines by up to 30%, a critical capability when capacity delivery speed determines competitive positioning in a market where 72% of Sydney's new supply is already pre-committed.

• Advanced Liquid Cooling and AI-Optimised Thermal Management Systems: The transition from air-cooled to liquid-cooled data centre architectures — driven by AI workload density — is creating new construction requirements and methodologies that are being optimised using AI-powered thermal modelling. AI systems simulate airflow patterns, heat dissipation characteristics, and cooling efficiency across facility designs to optimise the placement of cooling infrastructure, minimise hot spots, and achieve Power Usage Effectiveness (PUE) targets of 1.3 or lower as mandated by government guidelines. Delta Electronics' installation of 12 prefabricated modular cooling units in January 2024 demonstrates the shift toward AI-optimised, modular cooling solutions that can be rapidly deployed to support high-density AI workloads.

• AI-Driven Power Infrastructure Planning and Grid Integration: AI-powered energy modelling tools are becoming essential for data centre construction planning as grid connection timeline delays of 2-3 years in major Australian metros create critical path constraints. AI systems analyse grid capacity, renewable energy availability, battery storage integration options, and load forecasting to optimise power infrastructure design and facilitate grid connection approvals. With data centres currently consuming 5% of national electricity generation — projected to reach 8% by 2030 — and Australia's Energy Market Operator accounting for electricity demand from data centres to triple by 2030, AI-powered power planning is essential for ensuring that new facilities can secure adequate and reliable power supply.

• Digital Twin Technology and AI-Powered Commissioning: AI-powered digital twin technology is transforming data centre commissioning and operational handover by creating virtual replicas of facilities that enable comprehensive testing, scenario modelling, and performance optimisation before physical systems are activated. These digital twins integrate real-time sensor data with AI prediction models to identify potential failure points, optimise system configurations, and validate that constructed facilities will meet their design specifications for power delivery, cooling capacity, and redundancy. The technology is particularly valuable for Tier III and Tier IV facilities — which together represent the dominant share of Australian construction — where concurrent maintainability and fault tolerance requirements demand rigorous verification of complex redundant systems.

Australia Data Center Construction Market Trends

Hyperscale Campus Development and Institutional Capital Influx Transforming the Construction Pipeline

The convergence of hyperscale campus development by global cloud providers and massive institutional capital investment in data centre platforms represents the most significant trend reshaping Australia's data centre construction market, creating a construction pipeline of unprecedented scale and complexity. Blackstone's AUD 24 billion acquisition of AirTrunk in September 2024 — the largest data centre transaction globally — validated Australia as a premier data centre investment destination and unlocked significant capital for AirTrunk's expansion program, including the 354 MW MEL2 Melbourne campus approved for construction with initial power-on slated for mid-2026. Partners Group invested AUD 1.2 billion in GreenSquareDC, while the October 2024 acquisition of Global Switch Australia for USD 1.937 billion further demonstrated institutional investor appetite for Australian data centre assets. NEXTDC commenced construction on its 550 MW S7 Sydney campus — a multi-phase hyperscale build program delivering capacity through 2029 — while announcing the AUD 2 billion M4 Melbourne campus in June 2025 and partnering with OpenAI for a AUD 7 billion Sydney computing cluster in December 2025. CDC Data Centers broke ground on a hyperscale campus in Western Sydney's Marsden Park that will become the Southern Hemisphere's largest data centre, drawing more electricity than 140,000 homes. Project Southgate targets 1.8 gigawatts of capacity by 2028, while Project Meridien proposes a one-gigawatt AI facility south of Broome that would place Australia in the same gigawatt class as the world's largest data centres. Melbourne, with approximately half Sydney's capacity, is experiencing the fastest growth rate nationwide as operators including NEXTDC and AirTrunk develop major new campuses, with the Victorian government fast-tracking approvals to accelerate construction timelines.

Power and Energy Infrastructure Challenges Driving Construction Innovation

The critical challenge of securing adequate, reliable, and sustainable power supply for the rapidly expanding Australian data centre sector is emerging as the most consequential constraint — and simultaneously the most significant driver of construction innovation — in the market, as grid connection delays of 2-3 years in major metros force operators and construction firms to develop creative power infrastructure solutions. Data centres currently consume 5% of Australia's national electricity generation, with projections indicating this will reach 8% by 2030 as deployable capacity more than doubles from 1.3 GW to over 3,100 MW. Australia's Energy Market Operator is accounting for electricity demand from data centres to triple by 2030, creating urgent requirements for grid augmentation, renewable energy development, and on-site power generation that are reshaping the scope and complexity of data centre construction projects. The electrical construction segment's dominance at 55.7% of the market reflects the critical importance and cost intensity of power infrastructure in modern data centre builds, particularly as AI workload densities escalate from traditional 5-10 kW per rack to 30-60+ kW and emerging 80+ kW per rack configurations. Telstra and Accenture formed a AUD 700 million joint venture approved in April 2025, addressing the infrastructure and connectivity requirements of the expanding data centre ecosystem. Construction firms are increasingly incorporating on-site renewable energy generation, battery energy storage systems, and behind-the-meter power purchase agreements into facility designs to reduce grid dependence and accelerate time-to-power. The government's PUE target of 1.3 or lower is driving adoption of advanced cooling technologies including direct liquid cooling, immersion cooling, and rear-door heat exchangers that reduce the power overhead of thermal management, while simultaneously increasing construction complexity and cost. Firmus Technologies secured USD 327 million in funding in November 2025 for data centre development, reflecting the capital intensity of building power-optimised facilities that can meet both current demand and future AI workload scaling requirements.

Australia Data Center Construction Market Summary

• The Australia data center construction market was valued at USD 1.30 Billion in 2025 and is projected to reach USD 2.29 Billion by 2034 at a CAGR of 5.93%, with total occupancy expanding from 37 MW (2005) to 1.3 GW (2025) and projected to exceed 3,100 MW by 2030.

• Amazon committed AUD 20 billion by 2029 and Microsoft pledged AUD 5 billion, while Blackstone acquired AirTrunk for AUD 24 billion (September 2024) and OpenAI partnered with NEXTDC for a AUD 7 billion Sydney computing cluster (December 2025).

• Electrical construction dominates at 55.7%, with AI workloads driving power densities to 30-60+ kW per rack — up from traditional 5-10 kW — while data centres consume 5% of national electricity generation, projected to reach 8% by 2030.

• ACT & NSW leads at 37.4% regional share with 72% of Sydney's new supply pre-committed, while Melbourne is the fastest-growing market and construction costs range AUD 10-11/watt in Sydney and AUD 9.50-10/watt in Melbourne.

• NEXTDC commenced its 550 MW S7 Sydney campus and CDC broke ground on the Southern Hemisphere's largest data centre in Western Sydney, while modular construction methods are compressing build timelines by up to 30% across major projects.

Australia Data Center Construction Market Growth Drivers

Explosive AI Workload Growth and Cloud Migration Creating Unprecedented Capacity Demand

The explosive growth of artificial intelligence workloads — combined with the accelerating migration of Australian enterprises to cloud computing platforms — represents the primary structural demand driver for data centre construction, creating capacity requirements that far exceed the existing infrastructure base and necessitate sustained investment in new facility construction over the forecast period. AI adoption has the potential to contribute AUD 600 billion annually to Australia's GDP by 2030, generating massive demand for the computing infrastructure required to train, deploy, and run AI models at scale. The transition from traditional computing workloads requiring 5-10 kW per rack to AI training and inference workloads requiring 30-60+ kW per rack — with emerging GPU configurations reaching 80+ kW per rack — means that each megawatt of AI capacity requires fundamentally different and more expensive construction than traditional data centre builds. OpenAI's AUD 7 billion partnership with NEXTDC to build a large-scale computing cluster in Sydney, Amazon's AUD 20 billion commitment by 2029, and Microsoft's AUD 5 billion pledge are primarily driven by the need to build AI and cloud computing infrastructure in the Australian market. Enterprise cloud adoption is accelerating rapidly, with 80% of Australian businesses planning cloud migration within two years, creating sustained demand for colocation and hyperscale capacity across all major metropolitan markets. The IT and telecommunications vertical's 31.9% market share reflects the foundational role of technology infrastructure providers in driving construction demand, while financial services, healthcare, government, and media verticals are generating incremental demand as they migrate workloads to cloud environments and deploy AI-powered applications. Hyperscale customers account for roughly 80% of new demand in Sydney, driving the development of large campus-style data centres that require multi-year construction programs and billions of dollars in investment.

Institutional Capital and Global Technology Investment Fuelling Construction Pipeline Expansion

The massive influx of institutional capital and global technology company investment into Australia's data centre sector is creating a construction pipeline of unprecedented scale, providing the financial resources necessary to fund the multi-billion-dollar developments required to meet rapidly growing capacity demand. Between 2023 and 2025, companies announced data centre investments in Australia that could scale up to more than AUD 100 billion, transforming the country's digital infrastructure landscape. Blackstone's AUD 24 billion acquisition of AirTrunk in September 2024 — the world's largest data centre transaction — demonstrated the institutional investor conviction in Australian data centre assets and unlocked significant expansion capital. Partners Group's AUD 1.2 billion investment in GreenSquareDC and the AUD 1.937 billion acquisition of Global Switch Australia in October 2024 further validated the sector's investment thesis. Australia ranked second globally in 2024 as the most attractive destination for data centre investment, behind only the United States, reflecting the country's stable political environment, established rule of law, skilled construction workforce, growing renewable energy supply, and strategic geographic position as a gateway to Asia-Pacific markets. The formation of Data Centres Australia — a peak body launched following a two-year pilot between AirTrunk, AWS, CDC Data Centres, Microsoft, and NEXTDC — reflects the sector's maturation and its collective commitment to addressing the planning, energy, water, and workforce development challenges that could constrain construction activity. Macquarie Telecom's IC3 Super West expansion represents a AUD 350 million investment creating over 1,200 jobs, while its Sydney IC3 campus delivers 63 MW total IT load, demonstrating the scale of individual facility investments. State governments are actively facilitating construction through fast-tracked planning approvals — as demonstrated by Victoria's acceleration of NEXTDC's Port Melbourne campus — recognising data centres as critical economic infrastructure that attracts technology investment, creates construction and operational employment, and positions Australia as a digital economy leader.

Australia Data Center Construction Market Segments

The Australia data center construction market is comprehensively segmented across construction type, data center type, tier standard, vertical market, and region, providing a detailed framework for analysing growth opportunities and competitive dynamics across the data centre construction value chain.

• Breakup by Construction Type: The market encompasses electrical construction (55.7% share) and mechanical construction. Electrical construction dominates driven by the critical power infrastructure requirements of high-density AI workloads, including power distribution units, uninterruptible power supplies, generators, switchgear, and grid connection infrastructure.

• Breakup by Data Center Type: The market includes large data centers (44.3% share), enterprise data centers, and mid-size data centers. Hyperscale campuses commanded 60.13% of market share in 2025, with colocation providers holding 55.08% as operators like NEXTDC, AirTrunk, and CDC drive large-scale campus development.

• Breakup by Tier Standard: The market is segmented into Tier III (46.8% share), Tier IV, and Tier I and II. Tier III facilities dominate driven by their concurrent maintainability specification that allows maintenance without service interruption, while Tier IV facilities are the fastest-growing segment at 5.46% CAGR as mission-critical AI workloads demand fault-tolerant infrastructure.

• Breakup by Vertical Market: The market serves IT and telecommunications (31.9% share), banking/financial services/insurance, public sector, healthcare, media and entertainment, retail, oil and energy, and others. IT and telecommunications leads driven by hyperscale cloud provider expansion, while BFSI represents a high-growth vertical requiring Tier III/IV reliability for financial transaction processing and regulatory compliance.

• Breakup by Region: The market is segmented across Australian Capital Territory & New South Wales (37.4% share), Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia. ACT & NSW dominates with 72% of Sydney's new supply pre-committed, while Melbourne is the fastest-growing market with construction costs of AUD 9.50-10 per watt compared to Sydney's AUD 10-11 per watt.

Australia Data Center Construction Market Competitive Landscape

The Australia data center construction market features a competitive landscape comprising data centre operators commissioning builds, global technology companies developing hyperscale campuses, specialist construction firms, and critical infrastructure suppliers. Key players operating in the market include NextDC Limited, AirTrunk (Blackstone), CDC Data Centers, Macquarie Data Centers, Amazon Web Services, Microsoft, Google Cloud, Equinix, Stack Infrastructure, DCI Data Centers, GreenSquareDC (Partners Group), Multiplex, BESIX Watpac, Delta Electronics, Siemens, Telstra, and Firmus Technologies, among others. These companies compete through capacity scale, construction delivery speed, power availability, cooling innovation, tier certification, location strategy, sustainability credentials, and customer relationships to serve Australia's rapidly expanding data centre infrastructure requirements.

Latest News & Development in the Australia Data Center Construction Market

• December 2025: OpenAI partnered with NEXTDC to build a AUD 7 billion large-scale computing cluster in Sydney, accelerating AI infrastructure deployment in the Asia-Pacific region, while NEXTDC also commenced construction on its 550 MW S7 Sydney hyperscale campus.

• November 2025: Firmus Technologies secured USD 327 million in funding for data centre development, while the Victorian government fast-tracked NEXTDC's approximately AUD 2 billion Port Melbourne campus to accelerate data centre construction in Melbourne.

• June 2025: NEXTDC announced its AUD 2 billion M4 Melbourne data centre campus, while the Telstra-Accenture AUD 700 million joint venture was approved in April 2025 to address infrastructure and connectivity requirements of the expanding data centre ecosystem.

• September 2024: Blackstone acquired AirTrunk for AUD 24 billion — the world's largest data centre transaction — while Global Switch Australia was acquired for USD 1.937 billion in October 2024, demonstrating unprecedented institutional investor appetite for Australian data centre assets.

• 2024-2025: CDC Data Centers broke ground on the Southern Hemisphere's largest data centre in Western Sydney's Marsden Park, AirTrunk secured approval for its 354 MW MEL2 Melbourne campus, and Data Centres Australia launched as the industry's peak body with backing from AirTrunk, AWS, CDC, Microsoft, and NEXTDC.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

https://www.imarcgroup.com/request?type=report&id=24635&flag=E

𝗔𝗯𝗼𝘂𝘁 𝗨𝘀

IMARC Group is a global management consulting firm that helps companies in diverse industries achieve sustainable growth through data-driven insights, strategic advisory, and cutting-edge research. Our extensive portfolio of market research reports spans across multiple sectors, providing actionable intelligence that empowers businesses to make informed decisions, identify growth opportunities, and stay ahead of the competition. From healthcare and technology to consumer goods and heavy industry, IMARC's research capabilities cover a wide spectrum of markets, enabling clients across the globe to navigate complex market dynamics, capitalize on emerging trends, and drive long-term value creation.

𝗖𝗼𝗻𝘁𝗮𝗰𝘁 𝗨𝘀

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-631-791-1145